BAS editor William Chislett

Welcome to Spain’s election year. Municipal and regional contests take place in May, and a general election is due by the end of the year.

Campaigns will be close fought, and significantly influenced by the economy. The statistics reflect both well and badly on Spain’s minority Socialist-led coalition government. Ministers will highlight economic growth of 5.5% in 2022, significantly better than forecast. Their opponents will point to a projected slow-down in 2023 to between 1% and 2% – the result of falling consumption, shortages of raw materials and the tightening of financial conditions affecting both companies and households.

Rising energy bills pushed the 2022 inflation rate to 5.5%. Critics call that high, but the government’s supporters point out that it was the lowest in the EU. Economic output is expected to recover its pre-pandemic (2019) level later this year (GDP shrank 11.3% in 2020 and grew 5.5% in 2021), but job creation remains sluggish.

Nonetheless, the vital tourism industry (12% of GDP in a ‘normal’ year) is recovering. The number of international tourists last year was more than 71 million (a record 83.5 million in 2019), up from 19 million in 2020 and 35 million in 2021. Arrivals in the key month of July (9.1 million) almost equalled those in the same month of 2019.

Merchandise exports have also held up very well. They were 23.6% higher year-on-year in the first 11 months of 2022, at a record €357.1 billion. Companies succeeded in offsetting lower sales in the domestic market with greater sales abroad.

During 2022 the government approved a series of steps to help companies and households, including €16 billion in direct aid and soft loans, an increase in the minimum vital income, a cap on regulated gas prices until the end of 2023, a petrol rebate of €0.20 per litre (more targeted this year), a reduction in VAT on natural gas bills from 21% to 5%, and mortgage relief measures, such as extending loan repayments for more than one million households.

Energy security risks are relatively low because Spain has a limited dependence on Russian gas, a well-developed liquefied natural gas infrastructure and alternative energy sources. Also, the so-called Iberian mechanism allows Spain and Portugal artificially to reduce wholesale electricity prices by capping the price of gas used for electricity generation.

A windfall tax is to be imposed on power companies and banks, which is expected to bring in a total of €7 billion in 2023 and 2024. In similar vein, a new asset tax will be levied on residents with more than €3 million in wealth (around 23,000 people, ie 0.1% of all taxpayers).

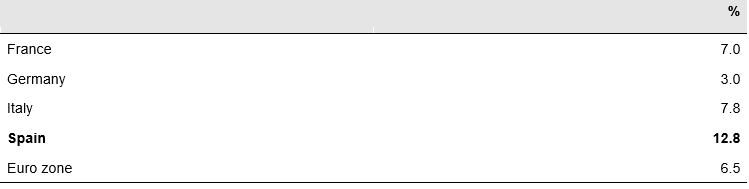

The number of jobholders now exceeds the pre-pandemic level. The 2021 labour reforms are increasing permanent employment, but the jobless rate was still high at 12.8% in 2022 (almost double the euro zone average), albeit down from 15% a year earlier and a whopping 24% in 2012 following the global financial crisis (see Figure 1).

Figure 1. Seasonally-adjusted unemployment rates, 2022 (%) (1)[1]

(1) November data except Spain which is the whole year.

Source: Eurostat.

Paradoxically, there are labour shortages, particularly in the hospitality and agricultural sectors. A government decree last July eased requirements for foreign workers without legal documents in order to bring them into the official labour force and make it easier for employers to hire workers from their home country. The Migration and Social Security Ministry estimates there are 500,000 people working in Spain’s underground economy.

Spain’s nine million pensioners are a politically important segment of a population that is fast ageing (average life expectancy is 82.3 years, above the UK’s 80.9 years). Unlike public and private sector workers, pensioners are maintaining their purchasing power. In fact, they gain in real terms as pensions rise by 8.5% in 2023, in line with the previous year’s average inflation as opposed to the year-on-year inflation rate of 5.5%.

The government restored the indexation of pensions to inflation in 2021, raising concerns about the system’s long-term sustainability if sufficient mitigating measures are not taken, such as extending the computing period for calculating pensions. Pension increases, coupled with the rising number of pensioners, account for around 30% of total government spending in 2023.

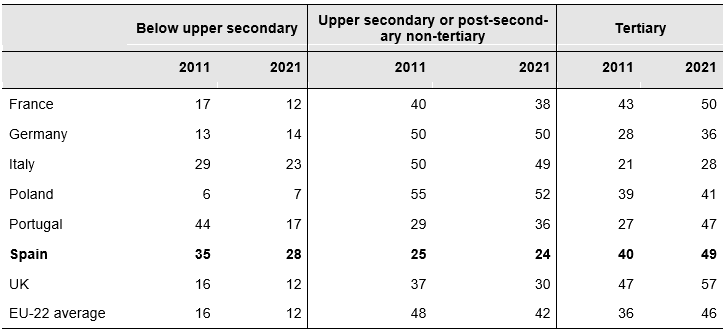

A long-term challenge is to boost labour productivity growth, which is lower than in peer economies. Vocational education reform should help enhance skills. While the share of tertiary-educated 25-to-34-year-olds increased from 34% in 2000 to 49% in 2021, at the other end of educational attainment 28% of this age group still only have the upper secondary education certificate, more than double the EU average (see Figure 2).

Figure 2. Trends in educational attainment of 25-to-34-year-olds, 2011 and 2021 (% of those with a given level at the highest attained)

Source: OECD, Education at a Glance 2022.

The €140 billion of the so-called Next Generation EU funds available for Spain, the second largest amount after Italy, should also spur economic recovery, though not as quickly as hoped. While the European Commission says Spain is implementing its plan on how to spend the money ‘in line with the agreed timetable’, only 22.3% of the €28.4 billion budgeted for 2022 had actually been paid out by the end of September, according to official figures. The Círculo de Empresarios, a business lobby, complains of a lack of transparency and capacity in the government to handle such a large volume of funds, of delays and of too much bureaucracy.

All in all, a challenging year ahead.

This article is an updated and adapted version of one published by the Elcano Royal Institute in December 2022.